Call it the end-of-summer ritual for investing nerds.

Every year in late August, the Federal Reserve Bank of Kansas City holds its Economic Policy Symposium. (Told you it was for nerds.) And every year at the symposium, the Federal Reserve chair delivers a closely watched speech.

As we sit on the cusp of the first interest-rate cut since the Fed started raising rates in March 2022, Jerome Powell’s speech at 10:00 a.m. ET tomorrow will be among the most watched and picked apart in years.

It will be watched closely because investors want clarity about rate policy – specifically that a cut is coming at the mid-September meeting.

It will be picked apart because odds are virtually 100% that Powell will not outright say a rate cut is coming. That means investors get to enjoy one of their favorite hobbies – reading the tea leaves to try to figure out what the “Fedspeak” really means.

While investors and pundits alike hang on every word to get a sense of what the future will bring in terms of interest rates, I don’t think what Powell says matters.

All the important data tells us it’s pretty much a foregone conclusion that September’s meeting will bring that long-awaited rate cut. The question at this point is more how big the cut will be.

And the question for investors is which stocks will benefit the most. (The answer follows.)

Rate Cuts are Imminent, Here’s Why

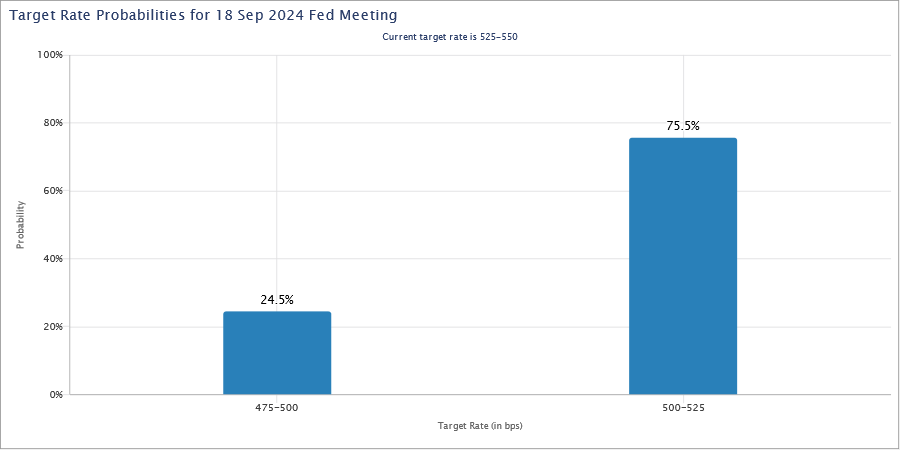

According to the CME’s FedWatch Tool, there is no chance that rates stay the same or increase. Investors view the probability for a quarter-point cut at 75.5%, with a bigger half-point cut having 24.5% probability.

Source: CME FedWatch Tool

I also believe this will be just the first in a series of cuts throughout the next 18 months, which may be about the best news for stocks we can get. Let me show you why.

The Fed is under increasing pressure from inflation data, the market, their peers, and a gross disparity between the Fed’s effective rate and market rates.

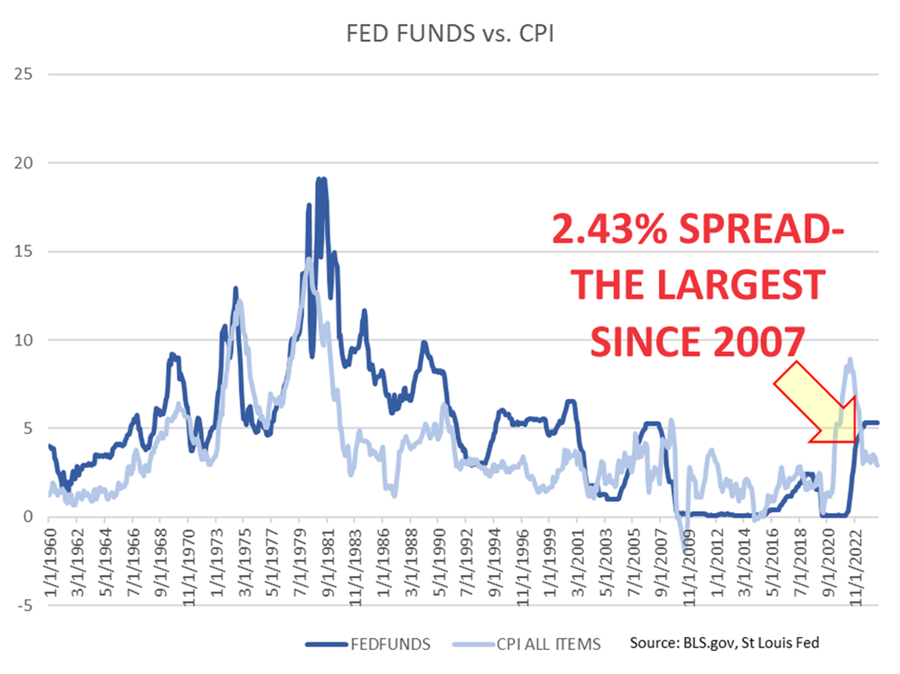

Let’s start by looking at interest rates versus inflation. The chart below shows the Effective Federal Funds Rate (EFFR) – which is real rates rather than policy rates – mapped against the Consumer Price Index (CPI), the Federal Reserve Bank’s preferred benchmark for inflation. The effective rate of 5.33% is substantially higher than the latest CPI report showing 2.9% inflation. That is the widest difference – or spread – on record since 2007.

Inflation is falling, but interest rates aren’t falling with it – something the Fed does not want. If the Fed waits too long to bring down rates, it increases the odds of a recession.

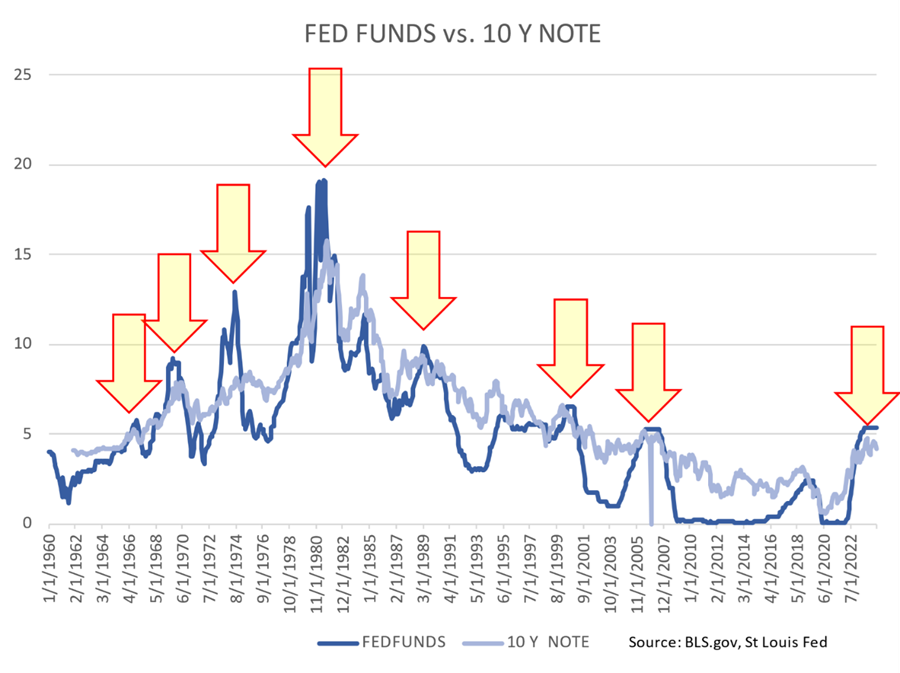

In addition, the Fed is grossly out of line with market interest rates. The best data source here is the yield on 10-year Treasury bonds, a very common benchmark to assess the market’s view of rates.

The chart below depicts the same EFFR of 5.33%, but this time plotted against the 10-year yield, currently at 3.79%. The spread between the two is 1.54%, which is unusually wide.

Even more relevant to right now, the Fed’s rate never exceeds the 10-year yield for very long. The natural state, on average since 1960, is for the 10-year note to yield more than the EFFR. We are now inverted, indicating the Fed is totally mismatched against the market.

A third reason the Fed has little to no choice is that central banks around the world have begun cutting rates.

In June, the European Central Bank (ECB), the Bank of Canada, and the Swiss National Bank all cut rates. And on Aug. 1, the Bank of England became the latest to join the party, voting to cut rates from 5.25% to 5%.

And last, but certainly not least, the Fed governors even said themselves that they would “likely” cut rates in September, according to minutes from their July meeting released just yesterday.

That’s overwhelming pressure from multiple sources, and the Fed doesn’t want that fight.

The big question now is what will the stock market do, and which stocks will be affected?

These Stocks Will Rise as Rates Fall

This question gets a little murky given that we are in an election year.

Simply put, a Trump victory would likely be good for small- and mid-cap stocks. Think the Russell 2000. He is generally pro small-business, pro real estate, anti-tax, and will pressure the Fed for faster cuts (though as I’ve said, that’s already likely to happen next month). This isn’t just an option. We saw all of this happen in his last term.

And what if Harris wins? We can expect similar stock action to what we’ve seen with the Biden administration. That administration was beneficial for large-cap tech. He was pro regulation and more aggressive with taxes.

But in general, stocks do well under both Republicans and Democrats. When it comes to interest rates, the difference becomes more pronounced.

My research suggests that small- and mid-cap stocks typically benefit the most from falling rates. As rates come down, companies can refinance debt to cost them less, which impacts their bottom lines quickly. Smaller companies typically grow much faster, making lower interest rates more of a tailwind.

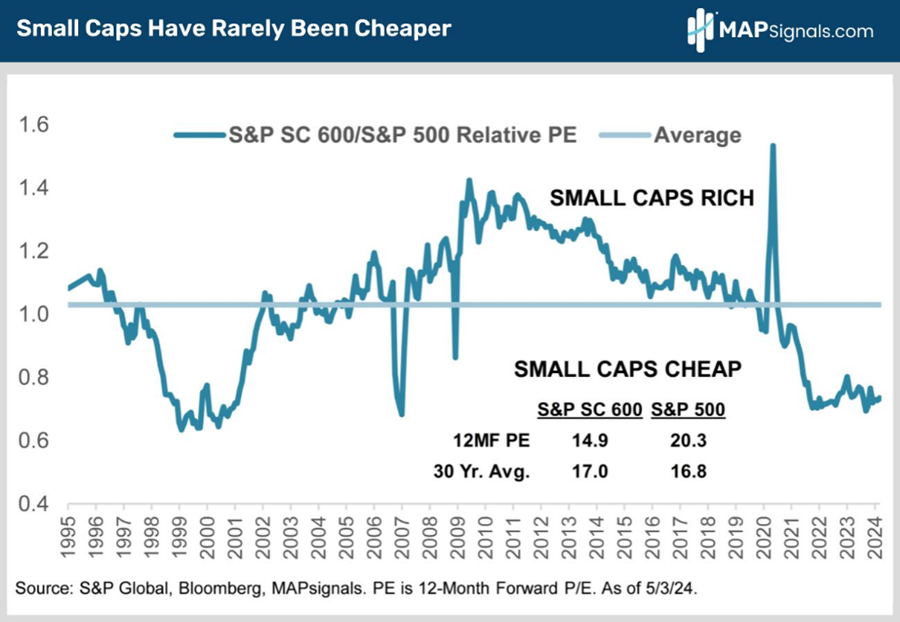

And as luck would have it, small-cap stocks have rarely been cheaper than right now, as measured by the PE ratio.

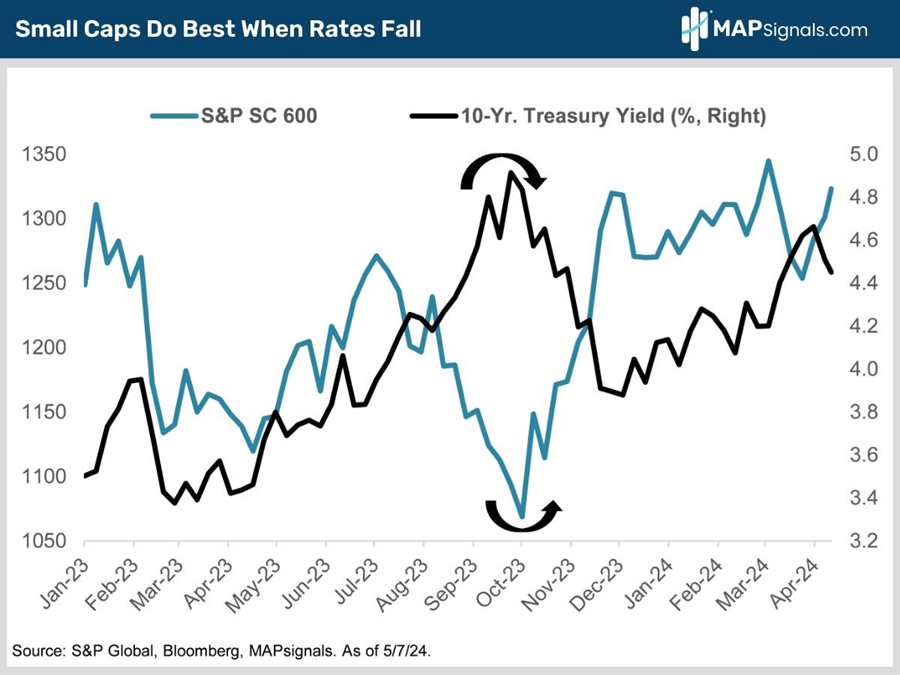

Small-caps tend to have an inverse relationship to interest rates. In the chart below, you can see small-cap stocks fall as rates rise. The 10-year yield peaked in Oct. 2023, and the S&P SmallCap 600 bottomed.

The opposite is also true – small-caps rise as rates fall. We’ve already seen the beginnings of that, and with the Fed about to cut, expect more juice behind these smaller stocks.

That doesn’t mean all smaller stocks will zoom higher. They are riskier by nature, which makes it even more important to focus on those high-quality stocks we look for with superior fundamentals, strong technicals, and those beautiful green lights (on my charts) that signal Big Money is buying in.

Talk soon,

Jason Bodner

Editor, Jason Bodner’s Power Trends